Developing a central bank digital currency (CBDC) system that supports offline transactions on smartphones or standalone custom devices will offer users benefits including enhanced resilience, accessibility, inclusivity and privacy, especially in remote areas without a reliable or affordable internet connection, according to the Bank of Canada.

The bank lays out the findings of its research into integrating offline functionality into a CBDC system in a staff analytical note that considers the advantages and drawbacks of two different design options that would allow for intermittent offline or extended offline operability according to the nature and extent of internet outage or lack of availability.

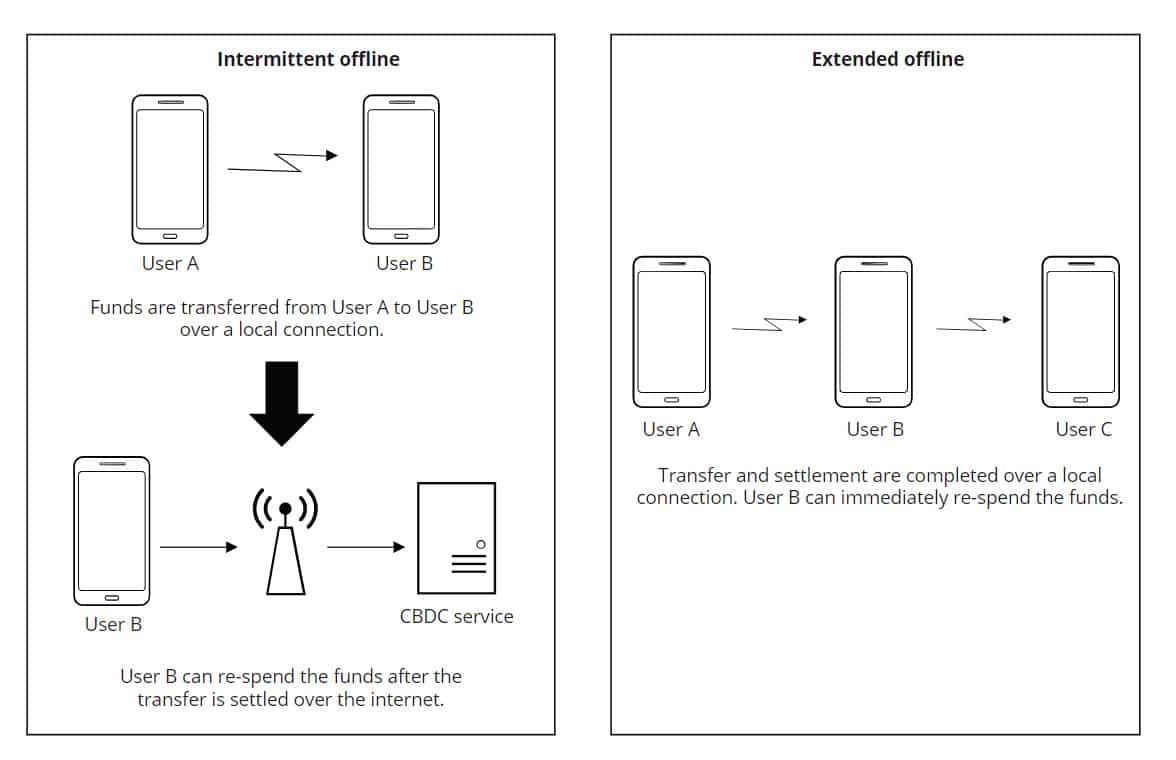

Design options

“An intermittent offline CBDC system could allow users to continue to transact during shorter, intermittent offline periods when the internet is temporarily unavailable. Offline capability in such a system augments an online CBDC solution,” the researchers explain.

“At the time of a transaction, the payee lays claim to a portion of the payor’s CBDC funds (clearing). The payor attests to this, thereby locking those funds from further spending by the payor.

“The actual transfer of funds (settlement) occurs later, when either the payor or the payee resumes connectivity with the online system. Since the online CBDC system records the final state of transactions and balances, settlement is deferred until internet connectivity resumes and the system updates.

“An extended offline CBDC system could allow users to transact during longer offline periods, when an internet connection is persistently unavailable or undesirable.

“An extended offline system is a distinct ecosystem supported by dedicated devices with a local store of funds. Devices with extended offline functionality can perform peer-to-peer payments without being connected to the internet.

“Funds are settled at the end of the transaction, ensuring that the payee is the sole owner of funds at the end of the transfer. Funds are also transitive — the payee can spend them in a follow-on transaction without waiting to send or receive an update from the remote service.

“Users could use an extended offline solution as a primary financial vehicle for day-to-day transactions.”

Security

In addition to identifying the key benefits to users of offline CBDC functionality as “enhanced resilience and better accessibility features” and “the privacy typically associated with offline payments”, the researchers note that a system supporting offline transactions will require developers to address security challenges.

“To minimize the risk of theft or loss, an offline CBDC may require security hardware with controls to guard against unauthorized tampering, as well as a user-specific personal identification number (PIN), password or biometric authentication stored on the device itself,” the researchers say.

“A balance must be struck between compliance, security requirements and user needs. A suitable balance may be defined by optimally selecting limits on holdings, transaction amounts and the duration of offline functionality.

“Adopting a security posture in terms of limits, controls and functionality, where risks are sufficiently mitigated, is still a challenge for technology available today.”

In January 2020 the Bank of Canada formed a CDBC working group with five other central banks and the Bank for International Settlements that in October 2020 laid out a set of ground rules for the successful issuance of CBDCs.

Next: Visit the NFCW Expo to find new suppliers and solutions