A major investigation into US consumers’ attitudes to mobile payments has found that concerns over how well they would be protected against loss should an issue arise is now the major barrier to widespread adoption of the technology.

The findings are based on a nationally representative survey conducted by The Pew Charitable Trusts. This captured Americans’ experiences and opinions of a wide range of payment methods, including mobile payments, credit, debit and prepaid cards, cheques and money orders, and cash.

The researchers divided the results into respondents who had used a mobile payment method in the past year and those who had not.

They also conducted interviews with payment industry executives and performed a detailed analysis of 12 mobile payment providers’ practices and policies for storing, using and protecting consumer funds, and handling disputes.

Question of trust

Nearly 30% of survey respondents reported that they opted not to use mobile payments on at least some occasions because they were concerned about a potential loss of funds.

“Consumers trust protections on debit and credit cards more than those on mobile payments,” Pew says.

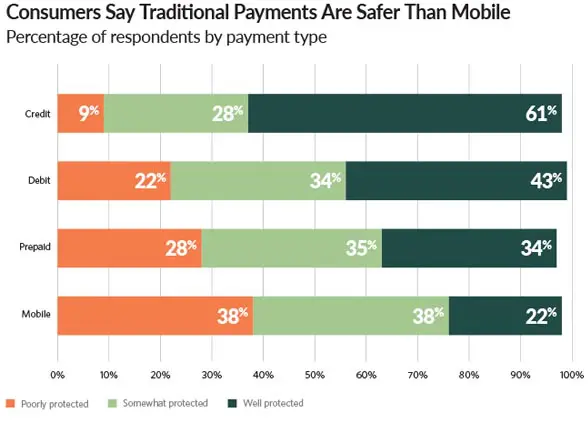

“Respondents were more likely to say mobile payments are ‘poorly protected’ (38%) than prepaid (28%), debit (22%) or credit cards (9%).

“This perception held even for mobile payments that involved a credit card and were therefore subject to the same financial safeguards as other transactions conducted with those cards.

“Just 35% of consumers said a mobile payment that uses a credit card was well protected, compared with 61% for a credit card on its own.”

Overall, 15% of consumers said they had experienced an issue with a payment method (mobile or traditional) in the past year. These problems included overpayment, disputes with a merchant and fraudulent transactions.

“Nearly all these consumers knew whom to contact to resolve their issue, were satisfied with the outcome and got their money back,” Pew reports.

But, while only 2% of mobile payment users experienced an issue with a mobile transaction in the past year, they were twice as likely as debit, credit and prepaid card users (39% compared with 20%) to report that disputes were difficult to resolve, and more than four times as likely (23% compared with 5%) to not know whom to contact.

Incentive needed

The lack of a strong incentive to switch from using cards to using mobile payments is also an issue, the researchers found.

“In public discourse and private discussions with Pew, some representatives from the payments industry suggest that this is in part because traditional methods simply work well enough to meet consumers’ needs while offering robust consumer protections,” they explain.

“For example, paying with the use of a smartphone at a point of sale is not materially easier than using a credit card.”

“Mobile payments have become part of the mainstream consumer finance market, but consumers nevertheless continue to use traditional payments with greater confidence and frequency,” the researchers conclude.

“Their hesitancy about mobile transactions is largely due to fear of loss of funds and because the advantages do not yet seem to outweigh the perceived risks.”

The full research findings are available to view on Pew’s website.

Next: Visit the NFCW Expo to find new suppliers and solutions

There are two big stumbling blocks to mobile payments in the US:

1) Lack of NFC chip ubiquity in the current generation of smart phones. Even Google sells non-NFC phones on its Google-Fi service that can’t be used with Google Pay for mobile payments!

2) The botched rollout of tap-and-pay at retail POS outlets. Many stores have the hardware in place with the tap-and-pay logo on it, but they don’t work in tap-and-pay mode.

Both attitudes and innovation in the US lag the rest of the world. That said, the rate of adoption of mobile payments in the US is currently unsustainably high.

While P2P mobile payments may not have good dispute resolution, those payments that involve banks are both more convenient and more secure.