A consortium of more than 70 leading banks, financial services providers and other businesses in Japan is to conduct a series of proof of concept (PoC) trials of a digital currency supported by commercial banks across a range of specific use cases with the aim of rolling the currency out by the end of the 2022 fiscal year.

The Digital Currency Forum began researching the options for the issuance and settlement of digital currencies in Japan in November 2020 and has now published a progress report and white paper with a “draft scenario” for a digital currency — currently known as DCJPY — and an interoperable two-tier digital currency infrastructure.

The forum is looking at “issuance and settlement methods for yen-denominated private-sector digital currencies” and says that it is also seeking to create an infrastructure that supports central bank digital currencies (CBDCs) and “cross-border instruments”.

Two-tier infrastructure

“It is assumed that the digital currency DCJPY will be issued by commercial banks as their liabilities, which are similar to bank deposits,” the white paper explains.

“The Digital Currency Forum also envisions that digital currency, DCJPY, will be able to connect organically with other digital platforms.

“In other words, the forum aims to realise a form of ‘digital payment as a service’, in which various economic activities and businesses can add payment and settlement functions as one of their wide-ranging services by incorporating the scheme of digital currency in accordance with their own business needs.”

“The activities of the Digital Currency Forum are not in conflict with the current discussions regarding stable coins and CBDCs. Rather they are complementary to each other,” the forum adds.

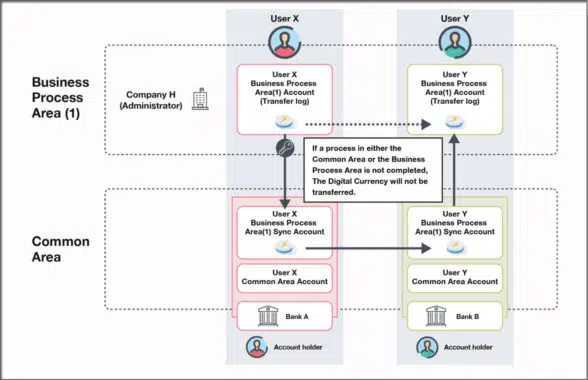

The two-tier infrastructure consists of a “Common Area” — “a structure shared by all the digital currencies issued under the scheme and will contain information on value and will be in charge of them for issuance and burn” — and a “Business Process Area […] responsible for the distribution of the digital currency”.

“So far, we have created a draft scenario for delivery versus payment settlement that straddles the Common Area and Business Process Area and possible goals and objectives the digital currency is expected to achieve,” the forum says.

“In the field of technology, we are actively promoting verification from various perspectives towards the realisation of digital currency issued by private entities, including the exchange of opinions among engineers in various fields and the mutual use of a sandbox environment for digital currency platforms.”

Use cases

According to the forum, some of the 10 sub-committees investigating individual use cases will be ready to implement PoC trials “by the end of 2021”. Use cases likely to be trialled include retail payments, supply chain transactions, industrial settlements, peer-to-peer and security trading, non-fungible tokens, e-money and regional currencies.

“Based on the result of the PoC, the sub-committees will continue our efforts to commercialize the digital currency DCJPY and the platform that supports its operation by the end of FY 2022,” the forum says.

The Digital Currency Forum is led by cryptocurrency exchange DeCurret with members including MUFG Bank, Sumitomo Mitsui Banking Corporation, Mizuho Bank, Seven Bank, NTT, East Japan Railway Company, Kansai Electric Power Company and Hitachi.

The Bank of Japan, Japan’s Ministry of Finance and a number of other government agencies are acting as “observers”.

The Bank of Japan announced that it was to begin concept testing a CBDC in October 2020, but said in October this year that “there is no change in the bank’s stance that it ‘currently has no plan to issue CBDC’.”

“However, while ‘issuing CBDC’ is a big decision, ‘not issuing CBDC’ is also a big decision as a move to seriously explore the potential for CBDC issuance is under way around the globe.

“If CBDC is not to be issued, we need to consider how to build payment and settlement systems suitable for a society that is becoming increasingly digital. In either case, maintaining the status quo is not an option.”

Next: Visit the NFCW Expo to find new suppliers and solutions