The Hong Kong Monetary Authority (HKMA) has completed the first phase of Project e-HKD to develop a digital Hong Kong dollar and in the process has identified three use cases where the adoption of a central bank digital currency (CBDC) could facilitate faster, more cost-effective and inclusive payments and enable new types of economic transactions.

In its Phase 1 Report, HKMA says that domestic and retail case studies carried out by a consortium of partner organisations “uncovered three key areas where an e-HKD could add unique value to consumers and businesses and address their evolving and future needs” and that “these are: programmability, tokenization and atomic settlement”.

Progammability

According to the report, “a programmable e-HKD could unlock new types of transactions for consumers and businesses, by facilitating the wider adoption of conditional settlements for retail transactions.

“This could create mutual incentives for transacting parties to complete the transaction in a timelier manner, which could be useful for certain interactions where consumers are used to paying in advance.

“An e-HKD could also facilitate ‘open loop system’ conditional settlements where related payment conditions can apply regardless of the means used to make the payment. This means transacting parties can benefit from conditional settlements without the limitation of having to use the same means of payment.”

Other benefits of incorporating programmable features into the proposed CBDC would include enabling businesses of all sizes to integrate and automate payment-related services such as vouchers, rewards and loyalty schemes and to facilitate the ring fencing and tracking of funds for specific uses.

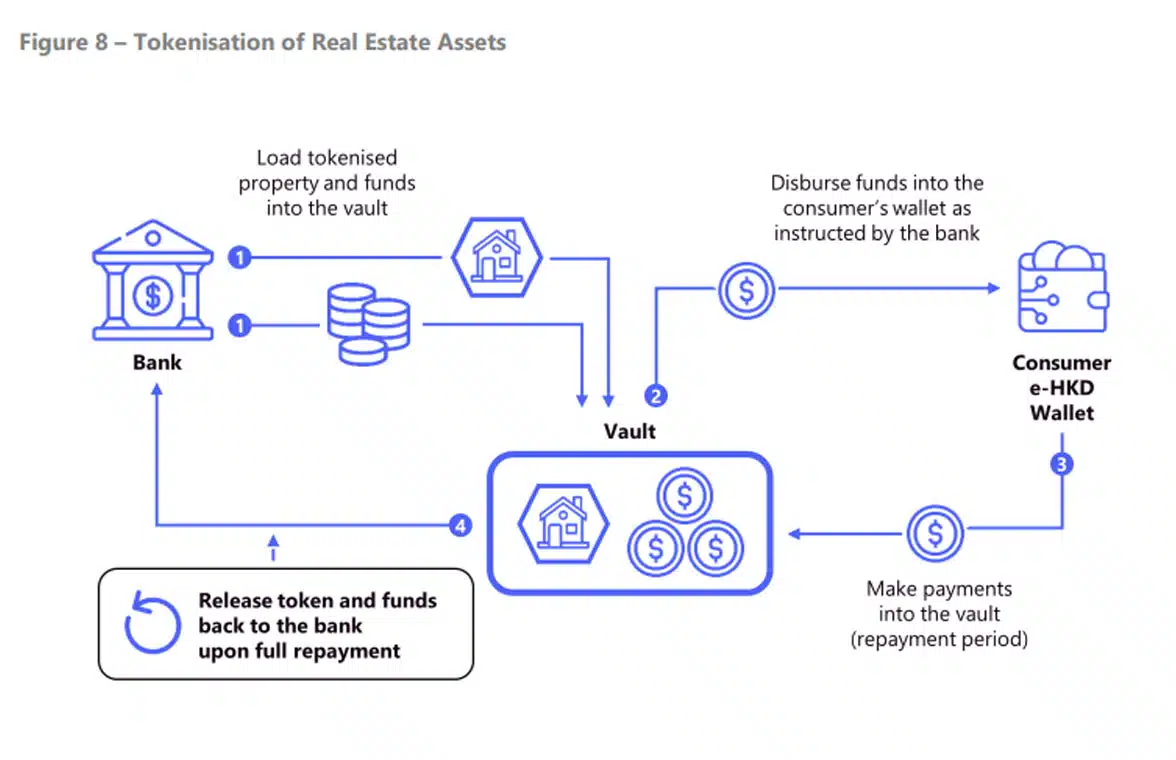

Tokenization

The pilot also found that an e-HKD “could eliminate the risk of conversion losses and volatility associated with cryptocurrencies and stablecoins”, and that, in relation to tokenized real world assets, it “has the potential to enable access to increased liquidity and accelerate the development of innovative token-based systems within the industry.

“This could lead to more integrated and faster ways of conducting core business activities.

“In one pilot relating to tokenized real estate assets, a hypothetical e-HKD was shown to enable faster approval of loans and consequently real-time, round-the-clock availability and automatic disbursement of funds.”

Atomic settlement

In relation to instant settlement, the project found that “an e-HKD could work in conjunction with the current set of financial infrastructure to enable a wider audience of consumers and businesses to enjoy the benefits of atomic settlement across a greater range of transactions”.

It could also “address last mile pain points which may be amplified in offline settings where consumers and merchants may lack perpetual access to an online network and are forced to handle settlements offline.

“For instance, dual offline payments via an e-HKD could help facilitate atomic transactions across offline and online contexts and enable an e-HKD to function as closely as possible to ‘digital cash’.”

Next steps

“The HKMA has not yet made a decision on whether and when to introduce an e-HKD. The outcomes and insights gained from Phase 1 of the e-HKD Pilot Programme will help enrich the HKMA’s perspective and refine its approach to the possible implementation of e-HKD,” the authority says.

“The next phase of the programme will seek to explore new use cases for an e-HKD and delve deeper into select pilots from Phase 1.”

HKMA launched the six first-round e-HKD pilots with support from 16 banks, payments and technology firms in May 2023.

Next: Visit the NFCW Expo to find new suppliers and solutions