A further four patent applications filed by Apple and relating to both NFC and mobile payments have now been published, clearly signalling that the company’s interest in near field communication technology goes well beyond simply making it easier to sync devices — and suggesting that the company may have major plans to develop its own mobile payments business.

A patent application filed by Apple in August 2009 and published today describes the use of an iPhone, or other electronic device, to make payments to other consumers or traders using the consumers’ choice of a credit or debit card, their bank account or credit stored in their iTunes account.

‘Peer-to-Peer Financial Transaction Devices and Methods‘ explains that, as well as P2P payments capability, the ‘electronic device’ could also use NFC to enable additional options:

A portable electronic device may be configured to store information representing one or more accounts held by a user. For instance, the stored information may represent one or more credit card accounts held by the user. As used in the present disclosure, the term ‘credit card’ shall be understood to encompass any type of card, including those in conformance with the ISO 7810 standard, such as credit cards, debit cards, charge cards, gift cards, or the like.

In one embodiment, a credit card may store a user’s account information using a magnetic stripe encoded on the card (e.g., ISO 7813 standard). In other embodiments, as will be described below, a credit card may include a storage device (e.g., in addition to the above-mentioned magnetic stripe) configured to store the user’s account information. The portable device may also be configured to store information relating to one or more bank accounts held by the user.

The portable device may also be provided one or more communication interfaces configured to send or transmit information stored on the device. For example, based on inputs or commands received from the user, the portable device may be configured to initiate payments (e.g., as a payor) by transmitting payment information corresponding to a credit account stored on the device, for example, to an external device (e.g., as a payee). In one embodiment, the receiving device may be a similar portable electronic device.

Additionally, the device may be configured to receive payment information from the external device and to initiate a transaction request in order to process the received payment information, such that a corresponding payment is credited to an appropriate account stored on the device (e.g., a bank account). For instance, the transaction request may include communicating with one or more external servers configured to provide an authorization for the requested transaction.

The electronic device may further include one or more input device, such as a camera device, as well as a plurality of communication interfaces, which may include a near field communication (NFC) interface.

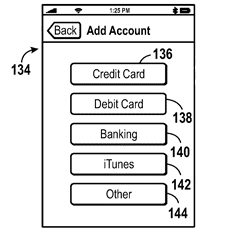

Images contained in the patent application indicate that Apple sees iTunes as one of the key types of account that could be used by consumers, with several of the figures clearly showing iTunes as one of the payments options, along with bank transfer, credit and debit card options.

A second patent application, filed in September 2009 and published on 1 April, looks more closely at the methods to be used to process P2P payments and describes the role of NFC in more detail. ‘System and method for processing peer-to-peer financial transactions‘ explains that:

Various techniques are provided for carrying out peer-to-peer financial transactions using one or more electronic devices. In one embodiment, a request for payment is transmitted from a first device to a second device using a near field communication (NFC) interface.

In response to the request, the second device may transmit payment information to the first device. The first device may select a crediting account and, using a suitable communication protocol, may communicate the received payment information and selected crediting account to one or more external financial servers configured to process and determine whether the payment may be authorized. If the payment is authorized, a payment may be credited to the selected crediting account.

Two further patents, meanwhile, cover the use of a ‘portable device’, such as an iPhone, as a mobile point of purchase or POS terminal, able to capture information about an item for sale, determine its purchase price and process payments.

‘Portable point of purchase user interfaces‘ and ‘Portable point of purchase devices and methods‘ were both filed in September 2008 and were published on 1 April. The patent applications both cover:

Handheld, portable, electronic, point of purchase devices configured to acquire identification information from articles to be purchased, to determine a purchase price, and to acquire payment information for the purchase price.

The point of purchase devices may include one or more input devices such as a near field communication device, a camera, a scanner, and a biometric sensor for acquiring the identification information and/or the payment information.

In some embodiments, the near field communication device may be detachable from the point of purchase device. The point of purchase devices also may contain communication interfaces, such as a near field communication interface, a local area network interface, a short message service interface, and a personal area network interface, for transmitting the information to an external server.

Next: Visit the NFCW Expo to find new suppliers and solutions