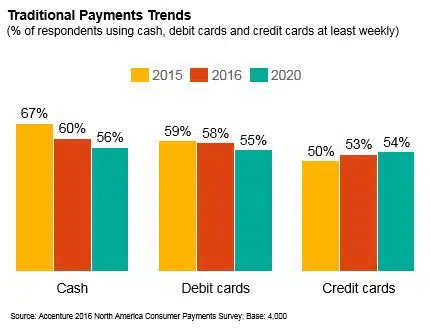

Nearly six in 10 North American consumers (56%) are now aware of mobile payment services — a 4% increase from this time last year, research from Accenture has revealed. However, the regular use of mobile payments remains flat at 19%, with 60% of consumers using cash at least weekly to make purchases at a merchant location.

The Accenture 2016 North America Consumer Digital Payments Survey, based on the responses of more than 4,000 smartphone users in the US and Canada, shows that consumers are expressing optimism about mobile wallet adoption in the future, anticipating a nearly 60% increase in the use of mobile wallets from card networks (14% in 2016 to 22% in 2020) and technology companies (13% in 2016 to 21% in 2020).

Of the nearly two thirds (64%) who have never used their mobile phone for in-store payments:

- 37% said they have not done so because they believe cash and plastic are fine for their payments needs;

- 21% prefer not to register payment credentials on their mobile phone;

- 19% are concerned that unauthorised transactions may happen.

Of those consumers who have used mobile payment apps in-store, consumers most frequently used their bank’s mobile app (26%) and 76% expressed satisfaction with this experience. Some 73% of the respondents said they trust traditional card providers the most as their mobile payments provider, followed by:

- Alternative payment providers like PayPal (63%);

- Established retail banks (62%);

- Large technology companies (59%).

When it comes to trying new ways to pay:

- 21% are interested in using wearables;

- 20% are interested in paying with smart devices to initiate payments;

- 30% are interested in the ability to park their car and have the car automatically pay for parking;

- 21% are extremely comfortable linking personal data with different ways to pay for faster authentication and one-step checkout;

- Nearly two in five are comfortable providing online bank account credentials to third parties.

More than half of millennials and mass affluent individuals (those earning $100,000 annually after tax) consider themselves to be among the first to try new technologies. Some 30% of millennials and 35% of mass affluents are “extremely interested” in initiating payments using wearables or smart devices.

The survey also found North American consumers’ use of debit cards for payments in merchant locations has remained consistent at 58%, while credit card usage was up 3% from the previous year to 53% in 2016.

Incentives ‘not there’

“We are seeing a gradual increase in consumer awareness of mobile phone payments options. However, adoption has remained flat over the past few years,” says Robert Flynn, managing director of Accenture Payments in North America.

“Consumers are content to use cash and plastic for everyday transactions and, while the use of cash is declining overall, it is the most commonly used form of payment — and consumers expect it to remain so in 2020.”

“The existing payments system isn’t broken, which is why consumers are not making a mass move to mobile phone payments adoption — the incentives are not there yet,” adds Michael Abbott, managing director of Accenture Digital and financial services lead in North America.

“Consumers expect more in today’s fast-paced digital environment — just the ability to tap and pay is not enough.”

Next: Visit the NFCW Expo to find new suppliers and solutions

“The existing payments system isn’t broken, which is why consumers are not making a mass move to mobile phone payments adoption — the incentives are not there yet,”

I argue that it is broken. However, that is a mere inconvenience to the consumer. Consumers will adopt mobile payments because they are more convenient, not because the card-based system is being held together with a band-aid. We will get the improved security as lagniappe.

3 years ago, I said

Mobile Wallets: Fix What’s Broken – And It Ain’t Payments

http://gtm360.com/blog/2013/11/01/mobile-wallets-should-fix-whats-broken-and-it-aint-payments/

Good to see it’s still the case, as reiterated by Accenture’s Michael Abbott.

Since I wrote that post, a number of retailers have replaced plastic loyalty cards with mobile phone #, so the “loyalty card replacement” use case I’d envisaged for mobile wallets in the post has also diminished in the meanwhile.