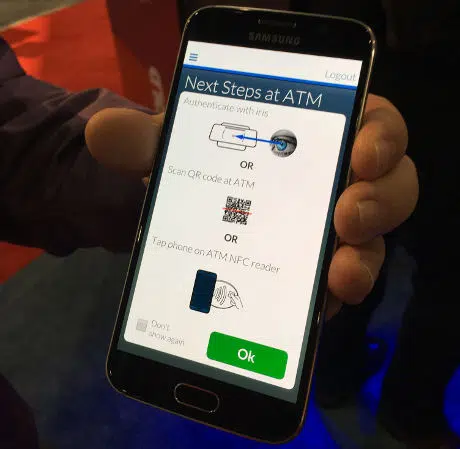

Citi has begun testing a screenless, cardless ATM concept developed by Diebold that lets customers make transactions using their mobile device instead of a plastic card and authenticate themselves using NFC, QR or an iris scan.

Customers using one of the new Irving ATMs download a mobile app and set up the transactions they wish to make when they reach the ATM on their mobile phone. They can then chose to have a QR code scanned by the ATM, tap their NFC phone against the ATM or have their iris scanned to authenticate themselves in order to complete the transaction they previously logged inside the mobile app.

“Cash withdrawals can be completed in less than ten seconds,” Diebold says. “Compared to a standard through-the-wall ATM, this terminal’s depth is reduced by as much as 32% and, on the consumer-facing side, it is up to 37% narrower when compared to other standard ATMs in the market.”

“Really, what this is aimed at is the tech-savvy individual,” Richard Harris, Diebold’s VP of new technology, incubation and design told NFC World during a product demonstration at Money20/20. “They do a lot of their banking online, they do a lot of banking on their mobile phone and this is a concept that really fits that particular consumer.

“We came up with this as a concept in the early part of the year and we had some meetings with Citi. We were focused, at that point, on mainly the NFC and QR aspect but when we started getting into discussions, they were really interested in experimenting around some biometrics as well.

“I think what you’re seeing a lot in the industry at the moment is a lot of ATMs are trying to enable for mobile. Being able to use the phone as a substitute for the card. What we’re thinking with this is how do the things complement each other, how do they work together to deliver the experience the consumer is looking for.”

Product range

“We’re working through productization around this particular unit,” Harris added. “Certainly from an NFC and QR code standpoint, we use that technology today in our existing products. The iris scanning is relatively new — we’re looking at making that more passive. That’s where we need to enhance it. Everything else, the NFC and QR code, there’s no reason why we can’t take that into a product range now.

“We’re having conversations with two more large banks in the US and one in the UK around some projects featured around this.”

The company is also demonstrating a second banking concept called Janus, a dual-sided, self-service terminal equipped with a tabletop touchscreen and an NFC authentication method for performing banking transactions that have also been logged by the consumer using their mobile device.

Diebold revealed last week that it has teamed up with HCE specialist SimplyTapp to offer banks a way to use their ATM network to add a layer of card present security to their mobile wallet provisioning process.

Next: Visit the NFCW Expo to find new suppliers and solutions

Magnetic stripe and PIN at trusted devices is the earliest and most successful example of strong authentication. However, as demonstrated by the dramatic increase in ATM fraud over the last few years demonstrates that it is clearly at the end of its useful life.

However Citi promotes this as an accommodation to changing customer preferences, it also illustrates the huge potential for improved security, not to mention cheaper ATMs, possible with mobile computers.

It is likely that, for reasons of backwards compatibility, we will live with magnetic stripe and fraudulent replay of credit card numbers for a decade or more. It is notable that this technology can coexist with legacy ATMs but the sooner we move to mobile, the better.